Star News

Phone new okof. Okof - all-Russian classifier of fixed assets

Depreciation groups and useful lives. Search for groups by OKOF code online.

The classifier of fixed assets is used to set the depreciation period for material assets and uses the codes of the All-Russian Classifier of Fixed Assets. For fixed assets put into operation since 2017, the useful lives are determined by the codes of the new OKOF OK 013-2014. For fixed assets commissioned before 2017, the terms are determined by the codes of the old OKOF OK 013-94. If, according to the new classifier, the fixed asset belongs to another organization group, then the terms do not change. For tax accounting, focus on paragraph 8, paragraph 4, article 374 of the Tax Code of the Russian Federation and paragraph 58, article 2 of the Law of November 30, 2016 No. 401-FZ.

Definition depreciation group and useful lives according to the OKOF code:

Classification by one table in MS Excel format, 51Kb Download

Depreciation groups:

- The first group - all non-durable property with a useful life of 1 to 2 years inclusive

- cars and equipment

- The second group - property with a useful life of more than 2 years to 3 years inclusive

- cars and equipment

- Means of transport

- perennial plantings

- The third group - property with a useful life of more than 3 years to 5 years inclusive

- cars and equipment

- Means of transport

- Industrial and economic inventory

- The fourth group - property with a useful life of more than 5 years up to 7 years inclusive

- Building

- Structures and transmission devices

- cars and equipment

- Means of transport

- Industrial and economic inventory

- worker cattle

- perennial plantings

- Fifth group - property with a useful life of more than 7 years up to 10 years inclusive

- Building

- Structures and transmission devices

- cars and equipment

- Means of transport

- Industrial and economic inventory

- The sixth group - property with a useful life of more than 10 years to 15 years inclusive

- Structures and transmission devices

- Dwellings

- cars and equipment

- Means of transport

- Industrial and economic inventory

- perennial plantings

- Seventh group - property with a useful life of more than 15 years to 20 years inclusive

- Building

- Structures and transmission devices

- cars and equipment

- Means of transport

- perennial plantings

- Fixed assets not included in other groups

- Eighth group - property with a useful life of over 20 years up to 25 years inclusive

- Building

- Structures and transmission devices

- cars and equipment

- Vehicles

- Industrial and economic inventory

- Ninth group - property with a useful life of over 25 years to 30 years inclusive

- Building

- Structures and transmission devices

- cars and equipment

- Vehicles

- Tenth group - property with a useful life of more than 30 years inclusive

- Building

- Structures and transmission devices

- Dwellings

- cars and equipment

- Vehicles

- perennial plantings

Hello! In this article, we will talk about the features of the new OKOF, which appeared in 2017 and continues to operate in 2019.

Today you will learn:

- For what purposes is the classifier used by groups of fixed assets;

- What changes have affected OKOF;

- How to correctly correlate the old and new depreciation periods.

Objectives of the OCOF

Each accountant at the enterprise is obliged to control depreciation charges for objects that are on the balance sheet of the enterprise. This helps to respond in a timely manner to depreciation of funds, as well as to upgrade existing equipment.

For these purposes, the all-Russian classifier for fixed assets of the organization was created. It is called OKOF and represents grouped assets by depreciation period.

OKOF plays the following role in the life of the enterprise, as well as the country's economy:

- Coding and systematization of available information in order to simplify accounting operations;

- Compliance with international standards in the field of business operations;

- Assessment of existing fixed assets (their size, important components and general depreciation);

- Improvement of calculations;

- Calculation of the most important internal coefficients of the enterprise associated with indicators of the effective use of fixed assets;

- Identification of the period of carrying out a thorough repair of worn-out objects of balance;

- Information equipment of organizations.

New classifier OKOF 2017

The OKOF, to which everyone has become accustomed for so long, has been operating since 1994. Since then, a lot has changed, and therefore required changes in some of the components of the standards. In this regard, a new OKOF appeared in 2017. Its new name is OK 013-2014.

However, it applies only to new fixed assets of the enterprise. If you already keep records, for example, for equipment, then you do not need to switch to new standards. This affects those assets that were acquired before December 31, 2016.

That is, the acceptance of funds on the company's balance sheet until 2017 allows you not to make adjustments even if the amortization period under the new rules differs from the previous ones. If the company is just starting its operation, then it must comply with the introduced standards.

The code classifier contains 10 main depreciation groups. Their composition and numerical designation have changed.

The changes affected the following features of accounting for fixed assets:

- Some objects have been moved to another group (their depreciation period has changed);

- The number of characters in the designation of assets increased from 9 to 12;

- About 500 assets have been moved to the Materials group.

Back in 2016, the limit for accounting for fixed assets for tax and accounting purposes was increased from 40,000 to 100,000 rubles. According to the rules of tax accounting, the cost of fixed assets, upon commissioning, was allowed to be written off immediately as expenses. According to the accounting rules, this OS must first be registered as a fixed asset and then its value transferred to costs through depreciation.

The next changes will affect movable property. If an organization has purchased vehicles on its balance sheet as fixed assets since 2013, then they were not taken into account as a tax base for calculation.

2019 will give local authorities the right to control this process by providing benefits to enterprises. If the regional administration does not provide such an opportunity, then you will have to pay funds to the treasury.

To determine which depreciation group the OS belongs to, you need to find in the OKOF the code that corresponds to it, then we find this code in the Classification and determine the group itself from the data.

If the object is not found, we are guided by the OKOF 2019 codes assigned to the groups of the highest level. How to use them? We replace the last digit of the code with zero, then discard two characters and do this until we find the desired code in the Classifier.

If the object is not in the OKOF and the Classification, then we determine its useful life, while being guided by the technical documentation (this can be a registration certificate, warranty card), then we set its depreciation group.

Old and new OKOF

To make it easier for you to understand the basis of the new OKOF classifier with depreciation groups, we have prepared a table. It correlates old and new OKOF values.

| Invalid OKOF | Designation | New OKOF | Designation |

| 130000000 | "Dwellings" | 100.00.00.00.000 | "Residential buildings" |

| 110000000 | "Buildings" (not including residential) | 200.00.00.00.000 | "Buildings" (without residential) |

| 140000000, 150000000, 160000000, 190000000 |

"Vehicles"; "Cars and equipment"; "Inventory"; "Other" |

300.00.00.00.000 | "Cars" |

| — | — | 400.00.00.00.000 | "Armament system" (for enterprises of relevant areas of activity) |

| 170000000, 180000000 | "Scot", "Plantings" |

500.00.00.00.000 | "Biological and cultivated resources" |

| — | — | 600.00.00.00.000 | “Costs for rights” (for example, for the use of the developed program) |

| 200000000 | "Intangible Fixed Assets" | 600.00.00.00.000 | "Intellectual property objects" (developments related to the use of own experience) |

As you can see, the equipment classifier was combined into a large group. New lines related to the existing rights of the enterprise also appeared.

For each group, the OKOF provides for the name of the object and its code. How to navigate here?

- the first three characters indicate the type of OS;

- the following indicate compliance with codes from the All-Russian Classifier of Products by Type of Economic Activity, approved by order of Rosstat on January 31, 2014 No. 14-st. The number of characters here can be from two to nine numbers, which depends on the length of the code in OKPD2;

- the fourth and fifth characters can take on a zero value if the OS does not have approved groupings in OKPD2 or another classification is needed in OKOF.

Download OKOF 2019 with transcript and search by name HERE

We are moving to the new OKOF 2017

With the advent of a new system of accounting for enterprise assets, accountants face difficulties. In order for the transition to the new classification to be successful, the state developed tabular data with transition keys, including OKOF codes with decryption.

Download transition keys

- direct transitional

- reverse transient

- If there is no corresponding name for the new classifier, choose the most appropriate one from the old one;

- Do not indicate compliance with old and new standards if, according to new standards, the name is excluded from the groups;

- Designate those names in the accepted all-Russian classifier of fixed assets that do not match in the old one;

- If you have any questions, please contact your operator at hotline, allocated specifically for employees of firms (phone numbers are publicly available).

At this time, there is a transitional classifier that has hints, and in order to correctly generate a report, follow a few steps:

- Find out if the code is correctly indicated according to the system in force before the innovations;

- Designate a new identifier according to the correspondence tables;

- Write down the information received in the inventory cards and note that the accounting took place according to the new rules;

- If you have already entered some asset on the balance sheet of the enterprise, then change only its digital designation;

- When attributing OFs to materials that are excluded from the new table, they must be transferred to the appropriate section. This applies only to those assets that have been received since 2017. Everything that was taken into account on the balance sheet earlier does not need to be transferred to the new groups;

- Select amortization period. If there are several suitable groups in the classifier for 1C, designate the one in which this period is the largest.

In order to systematize work at the enterprise, it is possible to issue an internal standard that will explain the norm of compliance of old and new designations in each case. This will avoid many inaccuracies and give justification for the expenses incurred by the company.

What is OKOF? The concept of the All-Russian classifier of fixed assets is familiar to all specialists responsible for accounting for enterprise objects. OKOF was developed for systematic work with funds or, which is the same in this case, fixed assets (OS). When compiling it, the standards and principles of accounting, statistical and international accounting were taken into account.

How it works? All enterprises in the process of activity, one way or another, acquire and use the OS. Each purchased item of property is assigned an individual depreciation group. The write-off period, that is, the use of fixed assets, depends on the code of the depreciation group assigned to them. This means that the cost of fixed assets according to the OKOF will be expensed within a certain period established by the enterprise.

Before 01/01/2017, classifier No. 359, approved by the State Standard in 1994, was used in accounting to attribute objects of ownership to certain depreciation groups of fixed assets. The document was very voluminous, so it was inconvenient to use. It has been in use for over 20 years and has been constantly updated. Despite this, the OKOF reference book has lost its relevance, and many definitions and signs of OS classification are outdated. Therefore, on January 1, 2017, a new one was put into circulation.

Main changes in OKOF

The latest OKOF reference system, which went into effect in 2017, has undergone major improvements and changes compared to the previous one. It was developed with a focus on international accounting systems: the codes of economic activity of enterprises (OKPD) were taken into account during development, the composition of depreciation groups and the period for writing off fixed assets have changed. The key changes in the new OKOF affected the structure of the codes - instead of nine characters, the codes now consist of twelve, and the composition of seven general groups.

The first 3 digits of the OKOF indicate belonging to the main group of fixed assets, and the rest - to OKPD2 according to CPA 2008 (to types of activities).

Basic OKOF codes

- 100/Residential buildings, premises;

- 200/Buildings, other than residential, structures;

- 300/Machinery and equipment as well. household inventory, and other objects;

- 400/Weapon systems;

- 500/Cultivated biological resources;

- 600/Expenses for the transfer of ownership of non-produced assets 700/Objects of intellectual property.

Subgroups have been created in each group, and a specific OKOF code has been assigned to each OS.

Transition to the new OKOF in 2017

When commissioning fixed assets acquired in 2017, enterprises should definitely apply the new OKOF. The principle of accounting for fixed assets acquired before January 1, 2017, on the contrary, should not be changed. Taking into account the depreciation for fixed assets put into operation until 2017, one should adhere to the previous procedure, that is, do not change the previously established write-off period.

For a comfortable transition to the new OKOF within the specified time frame, Rosstandart Order No. 458 of April 21, 2016 should be followed. The document presents a comparative table of "old" and "new" OS objects and the so-called "transitional keys". All information is presented in the form of a table, with which you can easily choose a new encoding for the OS.

The table indicates all positions that are currently not included in fixed assets, i.e. which do not need to be depreciated and transferred to the operating system.

In the new OKOF, many objects that were previously used as fixed assets, and for which depreciation was charged, are no longer classified as such. Actions with such funds are as follows:

- We clarify the correctness of the indication of the old OKOF code, valid until 2017;

- We set a new OKOF code using the transition key table (Order No. 458);

- We enter information into the OS inventory cards and note that the application begins on January 1, 2017. For property put into operation before 2017, retraining should not be done, it is only required to change the code values.

- If, according to the new procedure, property is classified as inventory, then it should also be transferred. But this, in turn, also applies only to objects that have arrived at the enterprise since the beginning of 2017. The OS put into operation earlier, but meeting these criteria, should not be transferred to the MPZ.

- We select a new depreciation group for fixed assets registered later than December 31, 2016. The service life of objects delivered before January 1, 2017 does not change. In the absence of a suitable code, a value of a higher level should be selected.

Loading the OKOF classifier for 1C 8.3 and 8.2

Since 01/01/2017, enterprises have been using both the "old" and the "new" OKOF. The “old” OKOF has already been loaded and is being used at work, but for all newly introduced operating systems in 2017, OKOF with new terms of use is used. To work properly with the OS, we need to download and switch to the new OKOF in 1C.

How to download OKOF in 1C

Consider loading the OKOF classifier into the 1C program using an example.

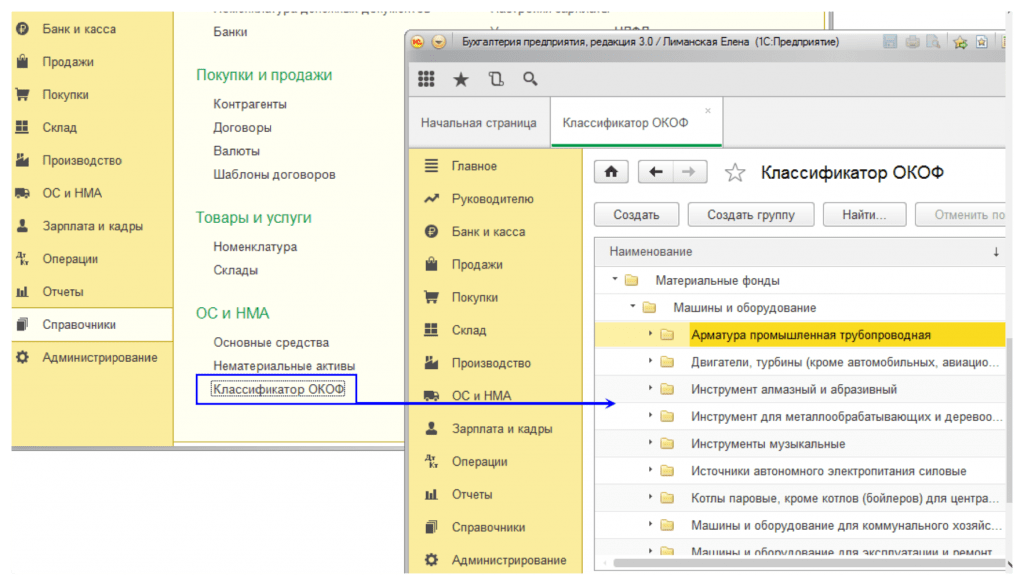

To update the OKOF in 1C Accounting 8.3, go to the "References" in the "Fixed Assets" section and find the desired document.

If the reference book “OKOF Classifier” is not displayed on the screen, you should add it to the menu using the settings (the settings button is presented in the form of gears).

A menu opens with a choice of actions from which we select the navigation setting.

On the navigation panel settings screen, select "OKOF Classifier", click "Add", and then - "OK".

As a result, in the "Directories", in "OS and NMA", the required "OKOF Classifier" will be displayed on the screen.

The program offers to open the file for download.

To download the OKOF update file in 1C 8.2, select a document previously downloaded and saved on your computer.

We click on it, and the 1C program starts downloading the file.

A message appears on the screen:

After the message disappears from the screen, you can proceed to upload the file to the program. To do this, in the lower right corner, click "Download".

At the end of the download, the screen will show “Download completed”, and the current “OKOF Classifier” will automatically be displayed.

New OKOF in 1C since 2017 for OS

Let's look at an example of how to choose a new OKOF code for the OS.

When filling out the OS card in the program, the OKOF code is filled in an empty field.

By filling in the OKOF code in the card, you can select information from two different directories: the “OKOF Classifier”, valid until 01/01/2017, and the “OKOF Classifier”, which entered into force after this period.

We select the desired depreciation group in the OKOF 2017 classifier.

We write down the data and draw the OS card.

OKOF update in 1C

To update the classifier, go to "References" again and select "OKOF Classifier".

In the Classifier and click "Load Classifier".

1C programmer consultation on our website or contact our specialists on .

From January 1, 2017, a new OKOF will come into effect. Within the framework of this material, the structure of the new OKOF and the procedure for the transition to its application are analyzed.

ABOUT The objects of classification in OKOF OK 013-2014 are fixed assets. Note that in accordance with the provisions of this document, fixed assets include produced assets that are used repeatedly or permanently over a long period of time, but not less than one year, for the production of goods and the provision of services.

FOR WHAT PURPOSES IS OKOF OK 013-2014 APPLIED?

For the purposes of accounting by public sector organizations, OKOF OK 013-2014 is applied in the cases provided for by federal standards, unless otherwise established by the authorized bodies of state regulation of accounting (introduction of OKOF OK 013-2014 (SNA 2008) in 2017).

Currently, Instruction No. 157n is in force. As follows from the provisions of this document (see clauses 45, 53, 67), accounting entities group fixed assets and intangible assets for the purposes of accounting (budgetary) accounting by types of property corresponding to the classification subsections established by OKOF. In other words, OKOF is used to determine the analytical account for accounting for fixed assets when they are registered.

IN WHAT CASES SHOULD OKOF OK 013-2014 BE APPLIED?

As noted in the Letter of the Ministry of Finance of the Russian Federation of December 27, 2016 No. 02‑07‑

08/78243, fixed assets accepted for accounting (budgetary) accounting as part of fixed assets before January 1, 2017 are subject to reflection in accounting (budgetary) accounting:

- in accordance with Instruction No. 157n, taking into account the grouping given in OK 013-94;

- taking into account the useful life of these objects, established by the Classification of fixed assets included in depreciation groups, approved by Decree of the Government of the Russian Federation of 01.01.2002 No. 1 (hereinafter referred to as the OS Classification) (as amended before January 1, 2017).

The grouping of fixed assets accepted for accounting (budget) accounting after January 1, 2017 should be carried out in accordance with the provisions of OKOF OK 013-2014 and the useful lives determined by the OS Classification (as amended by Decree of the Government of the Russian Federation of 07.07.2016 No. 640) .

WHAT STRUCTURE HAS OKOF OK 013-2014?

Note that OKOF OK 013-2014 includes 7 generalizing types of fixed assets:

- 100 "Residential buildings and premises";

- 200 "Buildings (except residential) and structures, land improvement costs";

- 300 "Machinery and equipment, including household inventory, and other objects";

- 400 "Weapon Systems";

- 500 "Cultivated biological resources";

- 600 "Expenses for the transfer of ownership of non-produced assets";

- 700 "Objects of intellectual property".

Some of the listed types of fixed assets are divided into subspecies, for example, type 300 “Machinery and equipment, including household inventory, and other objects” - into the following subspecies:

- 310 "Vehicles". Vehicles include vehicles designed to move people and goods;

- 320 "Information, computer and telecommunications (ICT) equipment". This equipment includes information equipment, complete machines and equipment designed to convert and store information, which may include electronic control devices, electronic and other components that are parts of these machines and equipment. In addition, such equipment includes computers of various types, including computer networks, independent data input-output devices, as well as equipment for communication systems - transmitting and receiving equipment for radio communication, broadcasting and television, telecommunication equipment;

- 330 "Other machinery and equipment, including household inventory, and other objects." This grouping classifies machines, equipment and devices that are not related to vehicles and ICT equipment, as well as household inventory (that is, items not directly used in the production process) and technical items that are involved in the production process, but not can be attributed to neither equipment nor facilities.

Each subspecies of the type of fixed assets also has a detail. For example, according to OKOF OK 013-2014, the subgroup "Machines for processing meat, vegetables and dough (equipment for mechanical processing of products at public catering establishments)" (code 330.28.93.17.110 OKOF) contains, in addition to the position "Kneading-mixing machines "(code 330.28.93.17.113) position" Equipment for the production of bakery products" (code 330.28.93.17.120).

HOW TO MAKE THE TRANSITION TO THE APPLICATION OF OKOF OK 013-2014?

In order to more correctly and quickly switch to the use of OKOF OK 013-2014, Rosstandart issued Order No. 458 dated April 21, 2016, which approved the transition keys between the editions of OK 013-94 and OK 013-2014. This document contains:

- direct transitional key, providing for the transition from the old OKOF

- (OK 013-94) to the new one (OK 013-2014) (volume 1);

- reverse transition key. It contains the transition from the new to the old OKOF (Volume 2).

Both transitional keys are presented in the form of tables, in which, for comparison, the codes and names of the positions of the old and new OKOF are given.

So, in the direct transitional key, each position of OKOF OK 013-94 corresponds to one or more positions of OKOF OK 013-2014. For example, the position “public toilets” (code according to OKOF 013-94 11 0001950) according to OKOF OK 013-2014 corresponds to code 210.00.12.10.810 “Toilet buildings”.

As officials of the financial department note in letters No. 02‑07‑08/78243 dated December 27, 2016, No. 02‑08‑07/79584 dated December 30, 2016, the commission for the receipt and disposal of assets of the organization can make an independent decision on attributing accounting objects to the corresponding group of codes OKOF OK 013-2014 and determination of their useful lives in the case of:

- the presence of contradictions in the application of direct (reverse) transitional keys and OKOF OK 013-2014;

- the absence of positions in the new OKOF OK 013-2014 codes for accounting items previously included in groups of material assets, which, according to their criteria, are fixed assets.

In addition, specialists of the Ministry of Finance draw attention to the fact that with the introduction of OKOF OK 013-2014 from January 1, 2017, during the transition period between financial years (inter-reporting period), operations to transfer the balances of fixed assets to new groupings, as well as operations to recalculate depreciation .

Tangible assets that, in accordance with Instruction No. 157n, relate to fixed assets, but were not included in OKOF OK 013-2014, are accepted for accounting as fixed assets with a grouping in accordance with OKOF OK 013-94. For example, by virtue of OKOF OK 013-94, stage clothing has code 16 3696601, however, in accordance with OKOF OK 013-2014, this accounting object does not apply to fixed assets. Due to this state-financed organization considers it as part of fixed assets on the basis of the old OKOF as production and household inventory on the account of the same name 0 101 06 000.

If, according to the classifier OKOF OK 013-2014, material assets are classified as fixed assets, but based on clause 99 of Instruction No. 157n, these assets are inventories (despite the fact that the useful life of these objects is more than 12 months), such objects are accepted for accounting in accordance with Instruction No. 157n as part of inventories.

For example, by virtue of OKOF 013-2014, wheelchairs (except for parts and accessories) belong to the main background type 310 "Vehicles", according to which they were assigned the code 310.30.92.20.

At the same time, in accordance with clauses 99, 118 of Instruction No. 157n, disabled equipment and vehicles for disabled people are classified as inventories and are subject to reflection on account 0 105 06 000 "Other inventories" regardless of their useful life. Thus, on the basis of paragraph 34 of Instruction No. 157n, the decision to register wheelchairs as part of inventories is made by the commission for the receipt and disposal of assets created in a budgetary institution.

In addition, it should be noted that low-voltage electrical equipment (up to 1,000 V), in accordance with the definition of fixed assets given in OKOF OK 013-2014, does not apply to fixed assets. Among them, in particular:

- switches, knife switches, control and protection relays;

- starters, switches, magnetic amplifiers, control chokes;

- distribution panels, lighting boards, cathodic protection devices.

* * *

Let us briefly formulate the main conclusions:

1. Since 2017, a new OKOF OK 013-2014 has been introduced. In order to provide practical assistance in the transition to the use of the new OKOF, transition keys have been developed that establish for each position of the current OKOF the correspondence to one or more positions of the new OKOF.

2. Fixed assets accepted for accounting as part of fixed assets before January 1, 2017 are subject to reflection in accounting (budgetary) accounting, taking into account the grouping given in OK 013-94 and the useful life established by the OS Classification (as amended by before January 1, 2017).

3. When taking into account new items of fixed assets acquired in 2017, one should be guided by OKOF OK 013-2014.

4. During the period of transition between financial years (inter-reporting period), operations to transfer the balances of fixed assets to new groupings, as well as operations to recalculate depreciation, should not be performed.

5. If, according to OKOF OK 013-2014, material assets are classified as fixed assets, but in accordance with Instruction No. 157n they are inventories, they are accounted for as inventories.

6. Tangible assets that, by virtue of Instruction No. 157n, relate to fixed assets, but were not included in OKOF OK 013-2014, are accepted for accounting as fixed assets with a grouping in accordance with OKOF OK 013-94.

Instructions for the use of the Unified Chart of Accounts for Accounting for State Authorities (Government Bodies), Bodies local government, management bodies of state non-budgetary funds, state academies of sciences, state (municipal) institutions, approved. Order of the Ministry of Finance of the Russian Federation dated December 1, 2010 No.? 157n.

Autonomous institutions: accounting and taxation, No. 2, 2017

From 2017, the life of fixed assets intended for depreciation will change. Since this year the new classifier OKOF (All-Russian classifier of fixed assets) 2017 will be relevant, and therefore, the accountant needs to make certain adjustments. These changes were adopted in accordance with the order of Rosstandart of December 2014. In this regard, the former classifier ceases to operate. As before, there are ten depreciation groups in the new version, but some of the assets have been transferred to other groups. At the same time, working with new OKOF codes in 1C is not at all difficult.

Recall what OKOF and ENAOF are in terms of 1C terminology.

Directory "OKOF"

The directory contains the all-Russian classifier of fixed assets. The directory is used to classify fixed assets when they are taken into account to determine the depreciation group. The OKOF code is specified for the fixed asset in the OKOF field.

Directory "ENAOF"

The directory contains a classifier of fixed assets, for which standard codes and annual depreciation rates are established. According to this directory, fixed assets are classified, for which depreciation is calculated according to ENAOF. For vehicles, depreciation rates are used as a percentage of the cost of the car per 1000 km of run. The ENAOF code is indicated for fixed assets in the ENAOF code field.

Download OKOF and ENAOF

So, in the folder with updates, after installing the next release of 1C, two files should appear: enaof and okof.

You can also download the okof.xml and enaof.xml files directly from our website. The files are suitable for any 1C configuration: Accounting, Integrated Automation, SCP, ERP.

- Download OKOF 2017 for 1C - file

- Download ENAOF - file

- Download OKOF in word - file

If you have downloaded the file from our site, then you need to unzip it before installation.

Install and download new OKOF and ENAOF

To update or install directly, go to the section called "References", then select "OKOF Classifier" in the "OS and NMA" section.

On the form, click the button "Load OKOF classifier"

After the window appears in front of you, click here "Select File", find the directory in which the classifier files are located, and select the okof.xml or enaof.xml file directly.

The new classifier is implemented as a directory with a hierarchy of elements, so you can select any item as a value.

For fixed assets that began to operate in 2017 and later, the classifier OK 013-2014 is available, it determines the appropriate position of these funds in the tax return. As for the old fixed assets that were introduced before 2017, the following parameters are saved here - the norm and the term. Only codes change. There is no specific correspondence between the new and old versions of the codes. For the transition, special keys are required, which are listed in the order of Rosstandart. The table for the transition from the old to the new OKOF can be viewed.

The ENAOF classifier did not change in 2017, but it still makes sense to check its relevance.

To load the ENAOF classifier, you must first click the "Open and read file" button, if necessary, set the "Overwrite objects" flag. After the file is read, click on the "Upload" button.